Featured

Table of Contents

- – What happens if I don’t have Level Term Life I...

- – How does Level Term Life Insurance For Seniors...

- – Why is No Medical Exam Level Term Life Insura...

- – Where can I find Level Term Life Insurance Pr...

- – What is the difference between Level Term Li...

- – What should I know before getting Low Cost L...

Adolescent insurance coverage provides a minimum of protection and could offer coverage, which could not be offered at a later day. Quantities supplied under such protection are generally restricted based upon the age of the youngster. The existing restrictions for minors under the age of 14.5 would be the greater of $50,000 or 50% of the amount of life insurance policy active upon the life of the applicant.

Juvenile insurance coverage might be offered with a payor advantage biker, which attends to waiving future premiums on the youngster's plan in case of the death of the individual that pays the costs. Senior life insurance, occasionally referred to as rated survivor benefit strategies, gives qualified older applicants with minimal entire life protection without a medical exam.

The permissible problem ages for this sort of coverage array from ages 50 75. The optimum problem amount of insurance coverage is $25,000. These policies are normally much more costly than a totally underwritten policy if the individual certifies as a conventional threat. This kind of coverage is for a little face quantity, normally purchased to pay the burial expenditures of the insured.

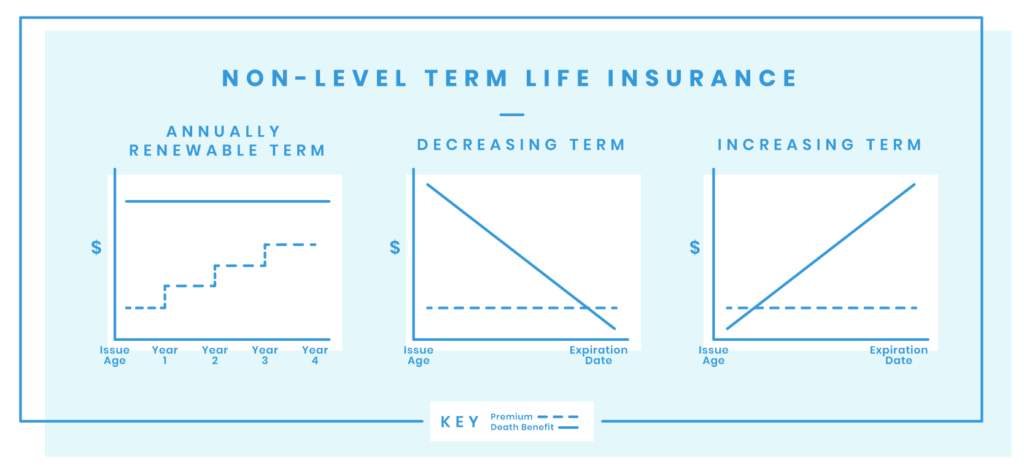

Our term life options consist of 10, 15, 20, 25, 30, 35, and 40-year plans. One of the most preferred type is level term, indicating your settlement (costs) and payout (fatality advantage) stays level, or the same, up until completion of the term period. This is the most uncomplicated of life insurance choices and needs really little upkeep for policy proprietors.

What happens if I don’t have Level Term Life Insurance For Families?

You might give 50% to your partner and split the rest amongst your grown-up kids, a parent, a friend, or also a charity. Level term life insurance policy. * In some instances the survivor benefit may not be tax-free, discover when life insurance policy is taxable

1Term life insurance policy provides temporary defense for a crucial period of time and is usually less costly than permanent life insurance policy. 2Term conversion standards and limitations, such as timing, may use; for instance, there may be a ten-year conversion benefit for some items and a five-year conversion opportunity for others.

3Rider Insured's Paid-Up Insurance coverage Acquisition Option in New York City. 4Not readily available in every state. There is an expense to exercise this motorcyclist. Products and cyclists are offered in approved jurisdictions and names and functions may vary. 5Dividends are not guaranteed. Not all participating policy owners are qualified for rewards. For choose cyclists, the condition puts on the guaranteed.

How does Level Term Life Insurance For Seniors work?

We may be compensated if you click this advertisement. Ad Degree term life insurance policy is a plan that provides the very same survivor benefit at any factor in the term. Whether you die on the very same day you obtain a plan or the last, your beneficiaries will certainly get the same payout.

Policies can likewise last till specified ages, which in a lot of situations are 65. Past this surface-level information, having a better understanding of what these strategies involve will help guarantee you buy a plan that fulfills your requirements.

Be conscious that the term you select will certainly influence the costs you spend for the policy. A 10-year level term life insurance coverage plan will certainly cost less than a 30-year policy since there's less opportunity of an incident while the plan is active. Reduced threat for the insurance company corresponds to reduce costs for the policyholder.

Why is No Medical Exam Level Term Life Insurance important?

Your household's age need to additionally affect your plan term selection. If you have young kids, a longer term makes feeling due to the fact that it secures them for a longer time. Nevertheless, if your children are near the adult years and will certainly be financially independent in the future, a shorter term may be a much better fit for you than a lengthy one.

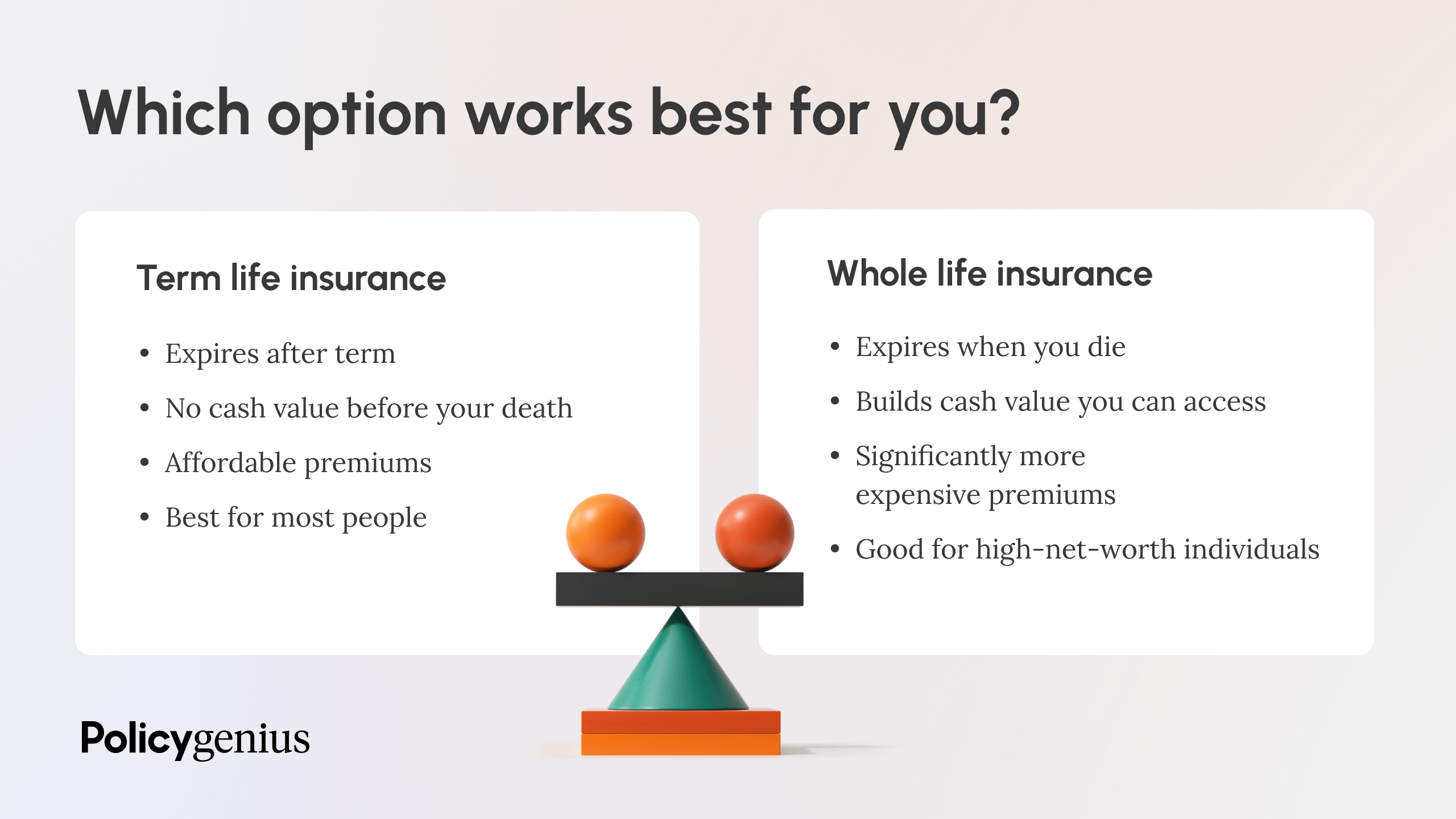

When comparing entire life insurance coverage vs. term life insurance coverage, it's worth noting that the last generally costs much less than the former. The outcome is extra coverage with lower premiums, supplying the ideal of both globes if you require a considerable quantity of insurance coverage yet can not manage a more expensive policy.

Where can I find Level Term Life Insurance Premiums?

A degree death advantage for a term plan generally pays as a lump amount. When that happens, your beneficiaries will obtain the entire amount in a solitary repayment, and that quantity is ruled out revenue by the IRS. Consequently, those life insurance coverage proceeds aren't taxable. Some level term life insurance policy business allow fixed-period repayments.

Passion payments received from life insurance plans are thought about earnings and are subject to taxes. When your degree term life policy ends, a few different points can occur.

The drawback is that your eco-friendly degree term life insurance policy will come with higher costs after its first expiry. Ads by Money. We may be made up if you click this ad. Advertisement For newbies, life insurance policy can be complicated and you'll have inquiries you desire answered prior to devoting to any type of plan.

What is the difference between Level Term Life Insurance For Families and other options?

Life insurance policy firms have a formula for computing threat utilizing mortality and interest. Insurance providers have thousands of clients taking out term life plans at the same time and make use of the costs from its energetic policies to pay enduring recipients of various other plans. These firms make use of mortality tables to estimate the number of individuals within a specific team will certainly submit death cases annually, which information is utilized to establish ordinary life expectancies for possible policyholders.

In addition, insurer can invest the money they get from costs and increase their revenue. Considering that a level term plan doesn't have cash money worth, as a policyholder, you can't spend these funds and they don't provide retirement earnings for you as they can with entire life insurance coverage policies. The insurance firm can spend the money and make returns.

The following section details the benefits and drawbacks of level term life insurance policy. Predictable premiums and life insurance policy protection Streamlined policy framework Prospective for conversion to permanent life insurance policy Minimal coverage duration No cash money worth build-up Life insurance costs can enhance after the term You'll find clear advantages when contrasting degree term life insurance coverage to various other insurance policy kinds.

What should I know before getting Low Cost Level Term Life Insurance?

From the moment you take out a plan, your premiums will never transform, aiding you plan economically. Your insurance coverage won't vary either, making these plans efficient for estate preparation.

If you go this path, your premiums will increase but it's constantly great to have some flexibility if you wish to keep an energetic life insurance coverage plan. Sustainable level term life insurance policy is another option worth considering. These policies enable you to maintain your existing plan after expiry, supplying adaptability in the future.

{kind=link}

Table of Contents

- – What happens if I don’t have Level Term Life I...

- – How does Level Term Life Insurance For Seniors...

- – Why is No Medical Exam Level Term Life Insura...

- – Where can I find Level Term Life Insurance Pr...

- – What is the difference between Level Term Li...

- – What should I know before getting Low Cost L...

Latest Posts

Top 10 Final Expense Life Insurance Companies

Life Insurance Instant Quote Online Dallas

Funeral Insurance Plan

More

Latest Posts

Top 10 Final Expense Life Insurance Companies

Life Insurance Instant Quote Online Dallas

Funeral Insurance Plan